HOW TRADITIONAL BANKING COMPANIES COUNTER FINTECH WITH DATA GOVERNANCE?

The new digital environment as well as a tough regulatory climate force the financial industry to adapt its business model in order to meet the demands of investors, regulators and customers. Today we mainly want to address the aspects of customer experience that traditional bankers ought to reflect on copying – or even exceeding. Because actually, it is customer experience that could be the traditional bank’s biggest asset. By this we mean that traditional banks are a one-stop shop for a broad range of financial products and services. This could serve both as an advantage as well as a competitive weakness to FinTech startups. Many traditional banks are still organized into silos. With business lines for individual products and services that use separate information systems and do not communicate to one another.

To improve on the customer experience, banks must be able to analyze customer information (data) and make that data useful for both the business and the customers. This is basically what Fintech does. However, they first need to gather the data. Traditional banks with a good data governance program, already have those data. They should have an advantage and leverage that.

To counter the extreme effectiveness and customer experience brought by new Fintech startups, some financial institutions are already upping their tech game. They work on the improvement of the user experience, they provide more insightful data analysis and increase cybersecurity.

While these are all true and important for banks, we believe getting “insightful data” is a little underestimated. There’s no data insights without clean data. There’s no clean data without a strong governance.

Data governance is all about processes that make sure that data are formally managed throughout the entire enterprise. Data governance is the way to ensure that data are correct and trustworthy. Data governance also turn employees accountable for anything bad occuring to the company resulting from a lack of data quality.

The role of data governance in the bank of the future?

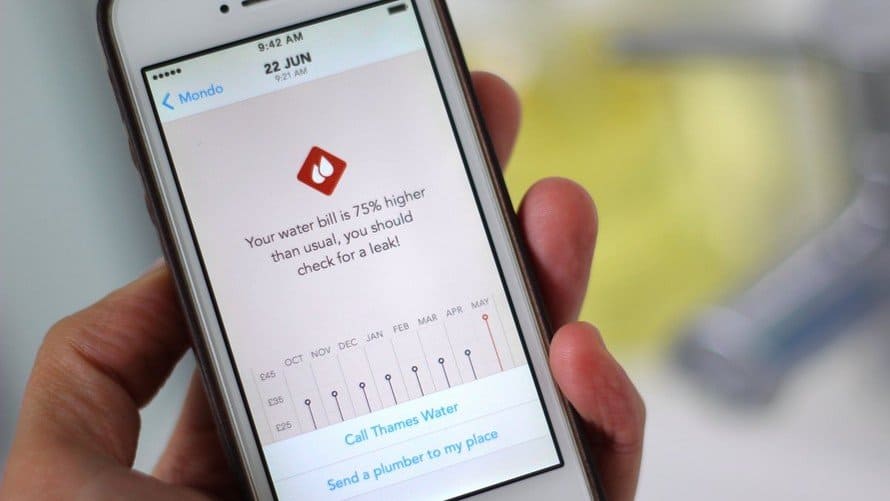

The bank of the future is tech- and data-driven. Today’s digital capabilities turn the customer journey into a personalized experience. The bank of the future is predictive, proactive and understand the customers’ needs. It’s some sort of “Google Now for Banking”, suggesting actions proactively. The bank of the future is a bank for individuals, it’s personalized in the range of services and products it offers to the individual – based on in-depth knowledge and understanding of the customer. By having up-to-date and correct data, you can truly serve customers.The “Bank of the Future” positions itself as ‘the bank that makes you the banker’. It thrives on interaction and a deep knowledge of its customers through data mining.

As the existing banking model is unbundled, everything about our financial services experience will change. In five to ten years, the industry will look fundamentally different. There will be a host of new providers and innovative new services. Some banks will take digital transformation seriously, others will buy their way into the future by taking over challengers and some will lose out. Some segments will be almost universally controlled by non-banks; other segments will be better within the structural advantages of a bank. Across the board, consumers will benefit as players will compete on innovation and customer experience. This is only possible with solid multi-domain, cross-silo data management with a solid data governance program on top of it.